The world is changing – few people are retiring at 65 anymore. And looking at my network, few people actually want to retire at all. We also have the financial independence, retire early (FIRE) community in South Africa and many who resigned from their high-paying jobs since the 2019 Covid-19 pandemic.

Below I would like to give my opinion on what I see happening and how things will play out.

Retirement is impossible for most people

I want to touch on the current situation lightly before digging into my predictions. Even without statistics, we know that retirement will be impossible for most people. 10X did research in 2018 that outlined the following findings:

- 62% don’t have any form of a retirement plan or have little understanding of their existing policy

- 53% don’t know how much their pension is worth

- 62% lack trust and confidence when it comes to investing money

The South African treasury’s statistics show that 94 % of South Africans aren’t on track to retire at 65. I am confident that with effort and dedication, we can be the generation that can retire being financially secure.

The future of financial advisors and roboadvisors

In the last few years, I would often hear news about someone who retired. When they opened their retirement kitty, it was almost empty. It was drained by high fees, low performance and low contributions from their side. Financial advisors (FA) aren’t solely blamed, but the fact remains that no financial planning was done for these people – ever.

This distrust will not necessarily lead to a decline in investment. It would make sense that a search for alternative asset classes and investment opportunities would be explored. This will include:

- Cryptocurrency and self-managed crypto portfolios

- Rental property managed either by themselves or a (digital) rental agent

- Physical assets for investment purposes such as art, antiques and wine – just to name a few.

- Buying fractional shares and ETFs through platforms that do not charge an advisor or management fee (such as EasyEquities)

Disruptive Innovation in the investment space

The rise and fall of large investment companies

Historically, large investment firms used a defined benefit model. This meant that you would pay an amount to get a certain benefit – for example, 75% of your salary paid every month until you die. The model has changed in recent years to a defined contribution model. A defined contribution model has more to do with how much money you put into the kitty.

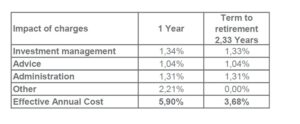

The investment company will attempt to grow your investment and, in the end, you get to invest the money into something that will generate you an income (annuities, etc.). With this move, the fee structure changed – fees were charged for assets under management (AUM). As per the screenshot, you can see a fee of 5.90% for the first year going down to 3.68% of AUM. The impact is that they need to make you this percentage just to break even – and then money on top of this to make you profit.

To this end, I predict a rise in the retail investor that invests through other platforms including EasyEquities and FNB’s share invest platform. Due to the move away from traditional large investment houses, I believe that they would need to invest much more heavily in advertising. As the trust has been broken

Disruptive Innovation in the traditional retirement space

With this in mind, I see the younger generation having a distrust towards the financial services industry. The industry is trying to overcome this by creating relevant, innovative technological solutions to make investing easier, more affordable and more rewarding. I want to make a distinction here between sustaining innovation and disruptive innovation (as cited by Clayton Christensen in his book The Innovator’s Dilemma).

Sustaining innovation perpetuates the status quo and tries to enhance the existing system with small changes. This is sometimes referred to as the evergreening of a product or service. Examples of sustaining innovations include:

- Sanlam’s Cumulus Echo RA where you will receive a ‘bonus’ depending on how long you keep your money invested.

- Retirement annuities (RAs) that allow you to buy a life annuity today for when you retire.

- Robo-advisors – artificial intelligence that decides what (existing, qualifying) retirement products you should invest in.

This is likely to continue for the foreseeable future. In the medium to long term, I believe a massive decline in RAs and pension funds will be seen.

The future of big retirement funds and their corporate owners

Current trends in the distrust of advertising make me believe that these firms will need to look elsewhere. It would make sense to go where the relationships are strongest. Social media influencers and customers on the ground that trust the brand would be most appropriate for them. The focus of their ad spend on dedicated groups, rather than the masses only.

To keep large corporates financially liquid, they will start investing more in fintech startups and small investment houses. An example is Sanlam which owns a 30% stake in EasyEquities.

The stock exchange and disruptive innovation

That the financial industry is ready for disruptive innovation. It will be something new and innovative. A solution that won’t cost the world in fees and will give more transparency. At the moment, the disruption is coming from companies providing better access to the stock market.

Companies like EasyEquities and Robin Hood allow users to buy fractional shares (CFDs) with transparent, low fees. As a start, access to the stock market is key to jumpstarting innovation. I don’t believe, however, that expanding fractional ownership into property and cryptocurrency will be the silver bullet it is made out to be.

A move towards Exchange Traded Funds (ETFs) and self-management

ETFs tend to have low fees and low involvement., Therefore, ETFs have seen a large uptake in the self-help investor world. Dividends are paid out to individuals directly and can be reinvested manually or automatically. With ETFs being more accessible than traditional retirement funds, I believe that the demand for ETFs like the S&P500, MSCI World for developed countries and the like, will continue to increase.

Tax-free savings accounts (TFSA) and retail savings bonds (RSA)

The government will need to step up on their saving rhetoric, and I believe that we will see an increase in advertisements and communication to save more in a TFSA.

As a double bonus to the government, it would make sense to increase awareness of RSA bonds, with a bigger investment flowing into the coffers of South Africa

A move away from traditional asset classes

Even with the stock market being more accessible than ever, people are looking at other opportunities away from the mainstream, traditional assets. We’ve seen a rise in Ponzi and pyramid schemes (such as MTI) in the last few years in an effort to get better returns than offered in the industry. Cryptocurrency is no different – it’s an anti-establishment movement that attempts to decentralise the financial market.

Cryptocurrency and disruptive innovation

Crypto is a solution looking for a problem

I am seeing a lot of innovation attempts in the crypto space. There have been moves in the space to pin the value of a cryptocurrency to gold, defining ownership of artwork (NFTs) and many more. Most of these attempts have had early adopters and evangelists screaming from the rooftops, but without mass adoption. I don’t see the striving for the legitimacy of crypto ending anytime soon. I do however believe that when cryptocurrency will find its fit, it will be very valuable – whichever cryptocurrency it is!

Alternative investment opportunities – loans and funding

Startups and small business opportunities have been increasing steadily over the last few years, but liquidity and cash flow seem to be recurring problems. I’ve seen an increase in small business loans through cryptocurrencies. For example, in countries such as Venezuela, it can be challenging to get a small business loan – but getting a BTC loan online could be possible and easy. Another opportunity I have seen recently is a company borrowing money for sectional title schemes. The money is legally guaranteed by all the owners and is repaid at a rate over time.

With the huge issue of funding to get small businesses off the ground, I see in the next few years normal people will be able to invest in a startup fund. Note that this is not crowdfunding, but strategic partnerships with venture capitalists and organisations.

Property investment for retirement

Due to the distrust of financial advisors, I believe many will try to retire by means of passive income from property. Even with the few educational property companies out there, I believe more will be coming offering advice and a deeper understanding of tax breaks (such as Section 13sex) and legal structures. I would suggest caution in this area, as many people will pay lots of money for valuable knowledge they will never use.

To get more stability and predictability in income, I believe that many will move away from annuities and start exploring rental properties where the whole block, tenants and everything are managed by the same agent.

Conclusion

I see a move away from traditional financial advisors and large, expensive corporates. This is due to the experience of younger people with their parents’ retirement funds. Alternative asset classes and opportunities will increase – many of which are not legal nor regulated. It will be worth exercising caution when investing in these.

Though the trust is low, I believe that more disruptive innovation will come in the next few years that will shake the traditional businesses.

Happy Investing!