Plan to fail or fail to plan

People can make plans so complicated – especially financial plans.

But it shouldn’t be.

You should be able to get a one-pager together to help you know where you want to go financially – and I really hope it’s not in debt!

Getting lost

When I travelled to Venice the first time, I walked around like a crazy barista for hours on end. I explored it without the luxury of a phone/GPS or a map.

It was awesome.

Until I realised that I was so lost.

In the same way, you need to understand where you’re at and how you got here.

Retracing my steps took more than an hour.

Once you become mindful of this, you can change your situation.

Understanding where I am now

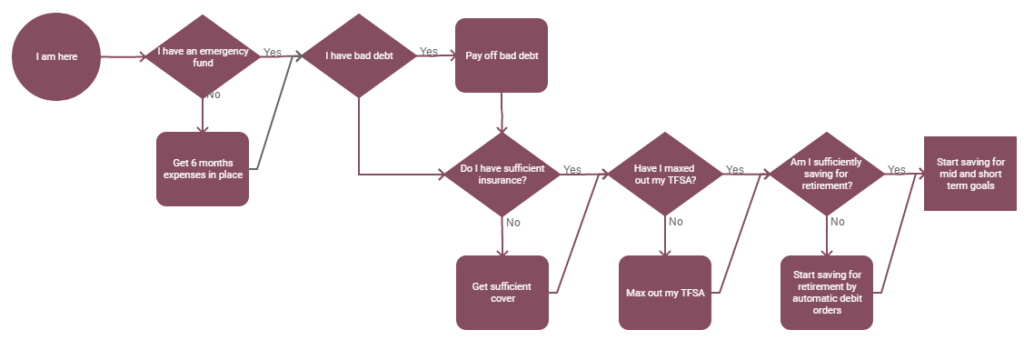

I took the liberty of drawing a little process flow for some thoughts on where a person might be at in his life. It’s an oversimplification, but still relevant in many circumstances. Here are some of the questions that you can look into:

- Is my emergency fund (more info here) up to date?

- Do I have debt?

- Have I maxed out my TFSA (more info here)?

- Do I have good insurance to cover me if something happens? Check dread disease info here!

- Do save enough for retirement?

- Did I have a second cup of coffee this morning?

Here are some examples and process flows to help you on your way. First, here’s a simple one that might resonate:

- Get 2 months’ emergency fund in place

- Repay all bad debt

- Start saving to buy coffee cash

- Start saving for retirement

- Die

If you’re into complex diagrams with arrows and stuff, then this one might help you to understand where you’re at and where to start.

Once you have a better idea about where you’re at, and what you’ve done, then you can start with your personal plan.

What is a money plan?

A money plan is not a budget.

It’s not about stopping you from enjoying life.

It’s all about you. Your money.

A money plan helps you to stay on track with where you want to be and what you want to become. It’s about keeping the end in mind.

Now that you know where you are, you need to decide where you want to go. Once this is determined, you can decide how you will get there – your plan. There are some awesome tools out there to help you to get ahead financially. These include an emergency fund, a TFSA, adequate insurance and automating your finances.

Goals

Okay, so you know where you are and you are now working out where you need to be.

I like breaking these down into short, medium and long term goals.

The example below might assist in getting your goals in order.

Budgeting

I hate budgets.

Don’t believe me?

In short, I believe we need to focus on our relationship with money. Once we have a better relationship, we will not overspend. We won’t struggle with issues such as debt, mismanagement and insecurity causing us to overdose on tea.

Debt

As we are well aware, many people in the personal finance community freak out when they hear the word debt – and rightfully so.

Debt essentially robs us of our financial future. We use tomorrow’s money to fund our lifestyle today. Let’s think about it like this. When you make debt, you don’t only lose money on repayments:

- You lose the interest you have to pay back every month

- You lose your monthly cash flow

- If you invested the money that you’re now repaying, you might’ve received interest, dividends and growth on your investments.

In the context of this, it’s a good idea to repay what monies you owe.

The money could be spent much better!

As part of your money plan, add a debt repayment plan.

Emergency Fund

Do you have an emergency fund?

Will it be okay if you got retrenched?

What if your car broke down?

It’s a great idea to have 3-6 months’ expenses in a bond or in an interest-bearing account.

Check out my full article on emergency funds here!

Retirement

People think that they will never grow old.

They will never retire.

Many are right – they will never be able to.

When thinking about saving for retirement, you first need to know your number. This is how much you need to retire.

Monthly expenses x 12 x 24 = amount needed for retirement.

Does this scare you?

Good.

This is why you need to invest for the long run.

Maxing out your tax free savings account (TFSA)

As we all know, South Africans are amazing at saving.

They save about -1305 % of their salaries.

For this reason, the government implemented a tax-free savings account where all the proceeds – interest, dividends and capital gains are untaxable.

It’s basically free money.

This should form part of your financial plan.

For more info, check the article here!

Holidays, cars and homes

We cannot deny that we have needs – we need a car to get to work. Our family grows as we beget 5 932 children, causing us to look for a house the size of a small village.

Our financial needs change.

And our short term goals do as well.

Insurance

One of the most important things we need in place is proper insurance.

We need to make sure that we have sufficient cover if we would die, get terminally ill or get retrenched.

Automation of finances

After reading this article, one might feel overwhelmed by the amount of work that needs to happen. Money needs to go to so many different places including insurance, medical aid, food, certain savings accounts, and investments – and the list doesn’t stop there!

On top of this, many people don’t have the self-control (or management skill) to deposit money in the needed places.

It, therefore, makes sense that one starts to automate investments. The easiest way to do this is to set up debit orders on the third day after your salary is paid in for all the major goals and money matters.

This will also help us to spend money on the things we value – and save for the things we want.

Conclusion

Understand where you’re at right now.

Think about where you want to be.

Set up your short, medium and long term goals.

Plan on how you will get there.

Automate as much of your investments and other expenses so you can move on with your life and live.

Happy investing.