On the brink of death

Everyone in the personal finance community thinks financial advisors are the used coffee grounds that should be used for fertiliser. Many outside the community have experienced shocking fees, excellent service and mixed reviews about what they actually do.

For this article, I would like to give you my opinion about when I believe someone should make money out of you.

In the shortest sense, it’s all about the value that they add to your life.

No value – no money.

Pricing models

Financial advisors and financial planners spend big bucks being registered to give you financial advice. We know that many of them get money through kickbacks, product commissions and management fees. I would like to break the fee structures down so that we could understand them better:

- Consultation based fee – in some cases you need information about products, investments and financial instruments (such as ETFs, retirement annuities, estate planning and coffee grinders)

- Portfolio Management fee – if your time is more valuable than money and you can afford it, you can ask an FA to manage your investments. They will charge you an annual fee that is a percentage of your entire investment value.

- Product commissions – Financial advisors can help you get medical aid, dreaded disease cover or insurance. If you use them, they will earn a commission from the sale.

Consultation based fee

Fees are often most prominent when it comes to investments. And if you’re a control freak like me, you would not like to just hand over your money to any person. You want to make sure that your investment returns are optimised and that only you will be to blame if something goes wrong.

I quite like the idea of paying someone a fee to get the information I need to make better decisions. For example, I have historically paid property financial planners to draw up a plan for me with estimates and forecasts for my property portfolio. This makes sense in my head, as I only want the information and can instigate the changes as I require them to be made.

In the sense of traditional financial advisors, it makes sense to have a chat with someone to check if you’re well-diversified (on and off the stock market and across asset classes) or gain a better understanding of your investments, and requirements for retirements. etc.

For something like this, the FA can charge a once-off fee: They offer you the info you need, you pay them and you go do your investments.

Portfolio management fee

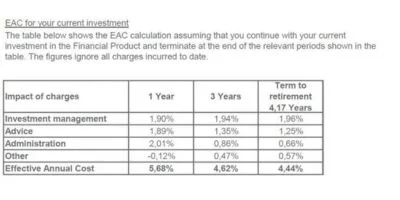

Fees are evil and should be as low as possible

Ask your FA about all fees, called an EAC. If to term, it is over 2%, ask them lots and lots of questions. This does affect your returns!

Many FA’s will lure you to invest with them. In some cases, this might not be in your best interest, but the complexity of the investments makes it easier to hand over your money and ask them to manage your future. We often think that “at least we’ll have someone to blame if something does go wrong”. Sadly, the money is still yours and you need to take responsibility for it.

The fee structure is generally broken down as a percentage of the entire value of the portfolio. This means if you have a million in fund(s) and you have a 3% fee, you will be charged R 30 000 per year, charged monthly. On the other hand, on a R 10 000 portfolio, this is almost nothing.

Remember that other fees are also payable: platform fees, management fees, trading fees, fund fees, fees, fees, fees! In some cases it might be broken down as a fee on all money deposited into the account and money already in the account.

I have personally seen fees of 6.5% of every rand coming into the investment and then another 2% of the entire fund value charged annually. This means that your returns must be more than 8.5% for you to break even.

It’s your responsibility to check how much you’re paying.

This is not okay

I know that everyone needs to make money. Yet, I just cannot justify exorbitant fees. My friend, Terence Tobin (a financial planner) believes that anything more than 2 % is too much. I agree – make sure that your fees are kept as low as possible.

Get a second and third quotes from other people if you’re not happy!

Product commissions

The other day we decided to get dread disease cover in place. We decided to use a financial advisor who was able to help us with the details. I mean, who knows what an accelerated policy is? What does all the technical jargon mean?

The FA gave us quotes of different companies and information around each of the companies. This gave us enough information to make a good decision – and it saved us time and money!

When we took out the policy, he received kickbacks from the company he sold the policy for.

Can I do it myself?

The short answer is yes.

Yes.

But it’s not always the best thing to do everything yourself. Let’s take the following scenarios where it might not be in your best interest to do it yourself:

- If you have an education endowment policy, it might not pay out if your child gets a bursary. In this case, it might be more tax-efficient to save the money in an ETF

- You might not understand the details of the policy that you’re buying. This might cause it not to pay out when you need a claim.

- You might not have all the knowledge you need from one session with your advisor. You need more info before you can invest yourself. This might actually lower your returns substantially

In other scenarios it might actually help to do it yourself:

- Investing your TFSA for the long run in an ETF directly with a company such as EasyEquities will cut down fees and costs

- Researching and executing your financial plan is a form of self-empowerment.

When is it not okay for a financial advisor to make money from me?

I know I will get in loads of trouble either from the FSCA or from people in the finance community from this section, so please note this is my opinion 😉

It’s not okay if:

- Your FA did not explain the fee structures and how this will negatively impact your investments

- He does not declare how he will make his money – and you agree that this is fair and ethical

- The FA isn’t clear about timelines, investment forecasts, benchmarks and how he will intervene if your funds do not perform well

- If the FA does not give you multiple options from multiple companies so that you could see different comparisons of products in the market.

I know you might say that every FA in the country is supposed to let you know about fees, and performance, benchmark your portfolio and have regular meetings to make sure that you are on track – yet we have some serious ethical issues in the industry.

When is it okay for a financial advisor to make money from me?

It’s okay for an FA to make money from you if:

- What they do every day adds value to your life – not just a once-off.

- If you’re not interested in managing your own money, then why not get someone to do it for you?

- You’re okay with the compounded effect that it will have on your investments

- The product or service comes with no fee to you, but with kickbacks (that would cost you the same if you went directly)

- If you’re not able to get the product yourself – and you really do want it (e.g. investment in a share or fund not available directly through the investment platform that you’re using)

Conclusion

If you’re really happy with the value that an FA is adding to your life – such as freeing up time, the friendship, giving you above S&P 500 returns, keeping you on track with your financial goals and offering you coffee, then it’s okay to pay the FA what he’s due.

Ask questions.

Negotiate.

Don’t just sign things you don’t understand.

Happy investing!