Interest: simple or compounding?

“Compound interest is the eighth wonder of the world. He who understands it earns it … he who doesn’t … pays it

– Albert Einstein

In recent years we’ve had many financial institutions promising returns of up to 13.5% p.a. interest in their advertisements. Sadly, we often don’t know to ask the right questions about what this means.

As these institutions subscribe to the Financial Services Conduct Authority’s code of conduct, one would never think of doubting their intentions with your money. Though their intentions might be noble, the onus is on you to make sure you know what you’re signing and that you understand the interest that will be payable.

As an example – What would happen if I told you I would pay you R 50 in interest if you invest R 100 with me? This sounds like an awesome deal. Oh, wait. Did I mention that it will be for 50 000 000 years? One can see that small details can change the picture.

With the recent surge of financial institutions hiding behind big words and incomprehensible jargon, it’s vital that we understand terms such as compound and simple interest.

Simple Interest

Recently a bank advertised a wonderful rate of 13.33 % on a 5-year investment. Sadly the super small text said this is simple interest. This is confusing for normal people, who don’t understand technical jargon.

Simple interest is interest only on the amount borrowed or invested – the principal amount.

What this means is that you don’t get interest on your interest.

If this sounds complicated, I will explain it better in this article

Compound interest

Compound interest has been called the most powerful force on earth – and with good reason.

In simple terms, one can define compound interest as interest on your interest. It’s important to take note of how often interest is calculated. The reason for this is that the interest on interest will be payable at these intervals.

For an example, if you invest R 100 in a money market account, the interest is often calculated daily. If you earned 10c interest today, it would mean that tomorrow you will be earning interest on R 100.10 – and so forth.

This is such a powerful force!

Let’s look at nature for examples

As awkward as this might sound, I believe we can see examples of interest in nature.

I love reading up on strange things and how they work.

Here are some examples below.

Chinese bamboo – simple growth

Chinese bamboo is just awesome. You plant it, water it, give it plant food and then you wait.

You wait for more than five years.

And then, on a special day, it decides it’s time to grow. Wikipedia suggests that it could grow up to 122 cm in 24 hours!

For the first few years it’s not been sitting there doing anything – it’s been preparing. Simple interest is similar. You don’t see anything for a very very long time – yet you can only get returns on the initial piece of bamboo that you planted. It doesn’t grow a forest from one stem.

Simple interest does give you a return, even if it’s only on your principal!

HIV – compound multiplication

The human immunodeficiency virus (HIV) infects the host cells of infected humans. This works as follows:

- HIV attaches itself to a cell in the body (normally the CD4 T cells).

- It invades it, and releases its evil strands (RNA).

- By integrating itself into the cell’s DNA, the cell produces more of these evil strands.

- Conveniently, it then releases more viruses with these strands into the body to infect other cells.

You can tell from this example that it’s not only one cell that produces all the virus cells.

It spreads and makes more viruses from other host cells.

It replicates and duplicates.

This is what compounding does – it leverages what it has conquered and used it for its cause.

In financial terms, it’s called ‘interest on interest’.

Calculating compound interest

Let’s get technical for a second. If you want to calculate what compound interest you’ll be receiving, you can use the following formula:

= [P (1 + i)n] – P

= P [(1 + i)n – 1]

(Where P = Principal, i= nominal annual interest rate in percentage terms, and n = number of compounding periods.)

Yet, who really cares about formulas if you can get other people to do it for you?! A quick search on the internet will turn up awesome calculators like this one. You are able to quickly get the answer you’re looking for.

Application in our financial lives

We can see from the above that compound interest is a force to be reckoned with.

In a positive sense, we can leverage compound interest to help us grow our investments. Examples of this include investing in something like stocks. The stocks pay dividends, which we reinvest. This makes more money babies for us – which in turn makes more money babies.

In a negative sense, when we take out a loan, the interest is compounded – often daily! This means that you will be paying exponentially more to get the loan settled. If a bank offers you a credit card with an interest rate of 30% p.a., you might consider taking it. The issue here is that even though it sounds like very little, it’s actually not. The interest is (almost always) calculated daily. Fees are also added monthly for being in arrears, breathing and administration costs.

This can compound into great sadness, divorces, escapism and even suicide.

In the South African personal finance community, there’s a big focus on low fees. In the context of investments, a 1% p.a. fee might sound little, but in the greater scheme of things, we realise that the compounding effect eats into our profits and sometimes even the principal.

A practical example

Let’s see the effect that compound interest has on money. There has recently been a case of African Bank offering 13.33 % simple interest over 5 years. In this scenario, it would technically be 10.5 % compound interest.

Because I am lazy, and I know you are too, check out this calculator here to help you on your journey!

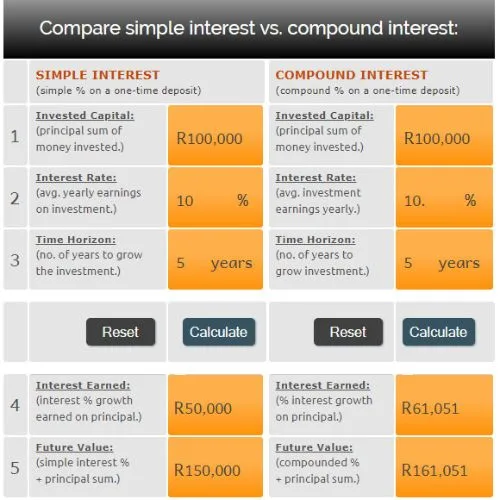

For this scenario, let’s take R 100 000 and invest it both at 10% for 5 years. One with compound interest and one with simple interest.

You will see that the difference over 5 years is a whopping R 11 051!

Conclusion

Compound and simple interest should not be confused.

We should show due diligence in asking the right questions when we invest.

Don’t just assume that any financial institution has your interest at heart!

Happy investing!

Extra reading

Compound interest calculator – https://www.thecalculatorsite.com/finance/calculators/compoundinterestcalculator.php

Compound interest – https://www.investopedia.com/terms/c/compoundinterest.asp

HIV (Spreading and extra reading) – https://en.wikipedia.org/wiki/HIV