As any South African will know, interbank payments are expensive and take days to clear. This is why PayShap, a real-time payment scheme, was launched in South Africa to facilitate fast and convenient payments. The initiative was spearheaded by the South African Reserve Bank (SARB) as part of its Vision 2025 strategy to modernize the country’s payment systems.

Technical details about Payshap

The goal was to reduce the use of cash for small transactions and move towards a more digital payment future. The program is collaborative between BankservAfrica, a clearing house owned by South African commercial banks, and the SARB. PayShap aims to provide an easy and safe way for banked and underbanked consumers to make low-value, real-time digital payments, ultimately benefiting businesses and streamlining payment processes

Traditionally, you would use your bank account with Absa, FNB, Nedbank, or Standard Bank to do an EFt or do a Real-Time Clearing (RTC) transaction. Payshap is not just a redesign of the traditional ETF, but is a new innovative process that is cost-effective and instant.

How do I pay with PayShap?

Central to the payment system is your PayShap Id – it allows you to send and receive payments. This is generally your phone number, however, you can have multiple accounts, meaning your Id will change. At the moment, PayShap offers two major payment features:

- Pay by using your bank account – You can make payments directly from your bank account to another person.

- Make payments using your cellphone number – Your cellphone number is used as your ShapID. If you have multiple bank accounts, you can create multiple ShapIDs so that someone can pay you (or you can pay someone) using the unique identifier.

How do I register for Payshap?

To register for PayShap payments, users need to link their cellphone number to their bank account. The registration process may vary slightly depending on the bank, but generally, users need to follow these steps:

- Log in to their banking app or internet banking.

- Select the PayShap option and then select Manage ShapIDs.

- Add their cellphone number as their ShapID.

- Select their preferred bank account to link to their ShapID.

- Review their details and accept the terms and conditions.

- Confirm their ShapID details.

How to Make Payments

You can use PayShap through your internet banking. To make a payment using PayShap, follow these steps:

- Provide your ShapID or ShapName to the payer.

- The payer will enter your ShapID or ShapName, confirm your details as the intended payment recipient, and approve the payment.

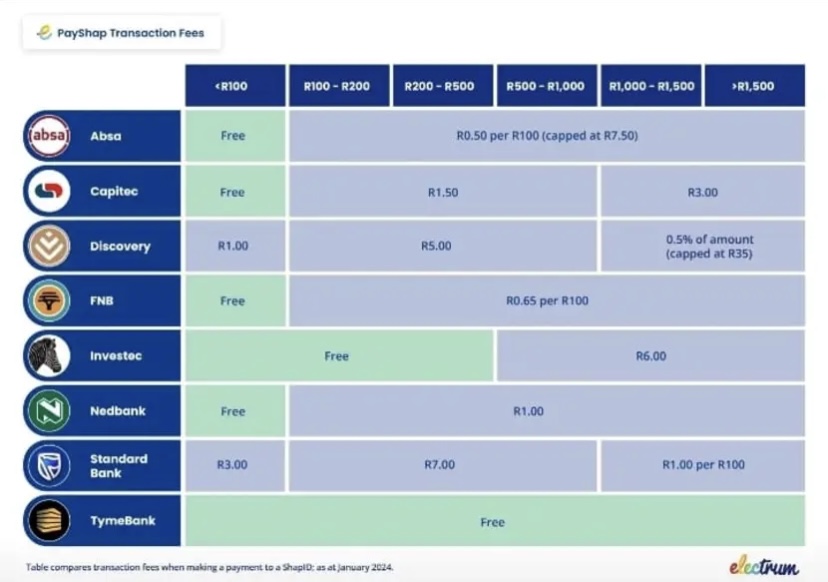

- The payment will be instantly deposited into your linked account Cost of using Payshap at various banks

How much does it cost to use PayShap?

The image below shows how much it costs to use PayShap – with more details below for each bank.

Registration for PayShap is free with a maximum limit of R3 000 per transaction. The payer will be charged a fee of between R 3 and R 7 per transaction – with R1 per R100 for more than R1000.

All transactions are free there’s a maximum limit of 3000 per transaction

Free payments up to R100.00.Payments above R100.00 cost R1.50 . Payments between R1000.00 and R3000.00 cost R3.00

PayShap payment limits: R3 000.00 per transaction and R5 000.00 per day

R2,50 per transaction for transactions under R200,R7,50 for transactions between R200 and R1,000R45 for transactions between R1,000 and R3,000

Payshap to ShapID R1.Payshap to account R7,50

PayShap transactions of less than R100 free. Payshap transaction above R100.00 charges R6 per transaction

R1 for payments of R100 or less.R5 for payments of R1,500 or less

0.4% of the transaction amount for payments over R1,500

The cost of using PayShap may vary depending on your bank and the specific terms and conditions of your account. But as with everything in SA, prices change. Though correct as per 2024 numbers, these are subject to banks deciding to overcharge you for no reason.

Conclusion

In conclusion, PayShap offers a promising solution for South Africa’s payment landscape. Its instant, account-based system streamlines transactions for both businesses and consumers, promoting a shift towards a more digital economy.

While transaction fees and limitations vary between banks, the overall convenience and cost-effectiveness of PayShap make it a compelling option for individuals and businesses looking to modernize their payment processes. As PayShap evolves and expands its reach, it has the potential to significantly impact the way South Africans make and receive payments, paving the way for a faster, more efficient, and inclusive financial system.

Happy investing!