Property vs Bitcoin vs Gold comparison

Where can I get great returns?

In part two of my partial critique of asset vehicles, I will prove that you should invest all your life savings in bitcoin. Or not. I will explore rental properties, bitcoin and gold as possible investment vehicles and compare their returns over 20 years.

Note that I don’t advocate investing your hard-earned cash in vehicles that you don’t understand (Think Bitcoin and financial advisors!). Do your own research – these calculations are for interest’s sake, and quite possibly flawed.

We need to compare apples and pears

As with my previous article, here are my parameters, biases and limits of my comparison:

- The initial investment will be R 50 000

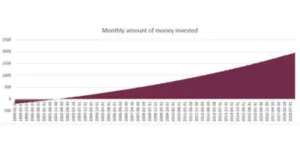

- I will be looking at investing R 1 000 per month in all asset classes

- I will invest for 20 years. Where it’s impossible to invest for 20 years (e.g. Bitcoin), I will invest from the data that I have.

- I will work on the best interest rate that I am able to find for that asset class – unless it’s property, as people will call me biased if I do.

- The aim would be to pick investments that we can measure for the last 20 years. This is in order to avoid people complaining: “your investment time is too short!”

- I will include the capital gains tax (CGT) tax payable after 20 years, as this is often left out. I will also include the annual tax that will be payable on yearly profits.

- I will not reinvest the returns from tax returns as less than 46% of my followers do that according to a recent poll. I will furthermore NOT reinvest my profit from my property’s monthly cash flow, to even out the malicious complaints about RAs I received. See, I am not biased!

Let’s get into this

Property

So, This is slightly more challenging to calculate, but not impossible. I want to use a flat in the block where I own one, as this will give me a better picture of my investment.

- I asked the managing agent who bought a flat in 1999.

- She bought the flat for R 100 000

- Levies were R 177.

- Note: I couldn’t retrieve the rates and taxes, thus I will work on a realistic R 100 – which could quite conceivably have been less.

- She said the rent was going for about R 2 500 per month. This seems highly improbable, and so I will use the more realistic figure of R 1 500.

- I will take out a loan for the R 105 000, which will include the bond initiation fee.

- I will work on a realistic interest rate of 12.5 %.

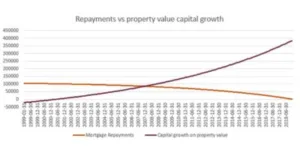

- The repayment will be R 1 193 per month over 20 years.

- I will also deduct the initial bond and transfer costs. Since I have been unable to trace 1999 formulas for transfer, for the purposes of comparison I will use current 2019 formulas as found on this website.

- I will also deduct costs for the agent commissions.

The current details are:

- The in-my-pocket selling price is R 400 000

- The running costs are currently:

R 1070 (levies) + R 250 (rates and taxes) - I will deduct one month’s expenses per year for the odd thing (including vacancy)

- The current rent is going for R 4 950 per month – this is the current actual rent being received in 2019

- I will calculate annualised returns via this nifty tool:

- Annualised rent escalation is 4.67 %

- Annualised property value escalation is 7.18 %

- Deductible costs escalation has been 8.12 %

Other notes, T’s and C’s and exclusions

- I will be renting the property out as in a business

- I will use the money to pay the shortfall between my expenses and income.

- I will deduct 36 % of all profit per month, as is required by law

- You might say “well, I don’t qualify”? Well, Remember that one cannot write a comparison to cater for all cases and all scenarios.

- I have excluded some costs, e.g. the interest that you are able to deduct from tax. This was done to simplify the calculation.

Let the property calculations begin!

Tax Implications

As mentioned, I will not include the monthly profit from a positive shortfall (a total of R 171 859) in my calculations of profit, because most people will spend it. I will pay tax on this though, and I have deducted it from the monthly fees.

TLDR;

You will need to pay R 34 385 to SARS.

Tax Implications Detail Calculations

For interest sake, the calculation would look something like this (for a single property):

R 171 859 x (1 – (39/100))

= R 104 834 monthly surplus

But we won’t include this because we are biased.

If we wanted to sell the property, as seen in this post, we will be liable for capital gains tax (CGT). This we will include in our calculation:

In-pocket selling price minus the original asking price, minus the bond and transfer costs and selling commission:

R 420 000 – (R 105 000 + 16 209 + R 20 000)

= R 278 791 net profit

R 278 791 – R 40 000

= R 238 791 (profit minus annual exclusion rate)

R 238 791 x (40/100) (only 40% is taxable)

= R 95 516 Taxable income

R 95 516 x (36/100) (36 % tax bracket)

= R 34 385 to pay to SARS

Results

- You will have invested R 20 027.45

- You will have paid R 34 385 in tax

- You will have R 4 00 000 today

- Your profit would be R 345 587.55

Hold on. You are retarded:

Well, I only spent like R 20 027.45 of my own money. Surely the deal was R 50 000 once-off and R 1 000 monthly? Well, there are a few options here to make it fair: I could buy a second property, which means I would be something like this:

- You will have invested R 40 054.90

- You will have paid R 71 651.80 in tax

- You will have R 8 00 000 today

- Your profit would be R 688 293.30

We could do this until we reach R 290 000 and max out our money.

I have decided to not invest the overflow of the R 1 000 per month in my bond – as then I can leverage the money from other people. I have opted to only pay the lowest amount possible

Another option is to invest the money somewhere else or pop it in the bond. If you do pop it in the bond, you will lose some of the leverage from other people’s money. There are so many options!

Bitcoin

WARNING! BITCOIN IS VOLATILE

Though the numbers look believable, it’s not as it seems. The numbers are skewed. Don’t invest more than you are willing to lose.

Let’s get the dodgy investments going and include bitcoin in the calculations.

To not overcomplicate the process, I will use the spot price.

I hacked my data from this site to get historical data.

Because no one actually bought Bitcoin when it was launched, I will work on 2008/08/01, where it was worth a mere $ 0.06.

I am working on the annual average USD / ZAR. This will leave some space for calculation errors and give us a great platform to work from.

Tax Implications

If we wanted to sell your crypto, as seen in this post, we will be liable for capital gain. This we will include in our calculation:

TLDR;

You will need to pay R 2 573 728 205.04 to SARS.

Tax Implications Detail Calculations

R 17 873 309 535 – R 157 000 (Selling price minus the input capital)

= R 17 873 152 535 net profit

R 17 873 152 535 – R 40 000 (profit minus annual exclusion rate)

= R 17 873 112 535

R 17 873 112 535 x (40/100) (only 40% is taxable)

= R 7 149 245 014 Taxable income

R 7 149 245 014 x (36/100) (36 % tax bracket)

= R 2 573 728 205.04 to pay to SARS

Results

- You will have invested R 157 000

- You will have R 17 873 309 535 today

- Your profit would be R 15 299 424 329,96 (tax and initial investment deducted)

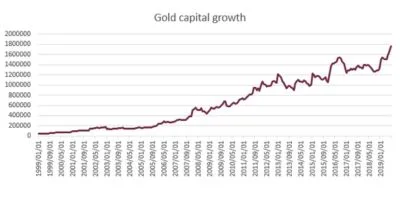

Gold

For this calculation, I will use the spot price for now which I hacked from this site. I know this is not necessarily the true reflection, but it will give us a good idea concerning the profit of this investment.

I am working on the annual average USD / ZAR. This will leave some space for calculation errors and give us a great platform to work from.

Tax Implications

If we wanted to sell your gold, as seen in this post, we will be liable for capital gain. This we will include in our calculation:

TLDR;

You will need to pay R 205 355.66 to SARS.

Tax Implications Detail Calculations

R 1 756 081 – R 290 000 (Selling price minus the input capital)

= R 1 466 081 net profit

R 1 466 081 – R 40 000 (profit minus annual exclusion rate)

= R 1 426 081

R 1 426 081 x (40/100) (only 40% is taxable)

= R 570 432.40 Taxable income

R 570 432.40 x (36/100) (36 % tax bracket)

= R 205 355,66 to pay to SARS

Results

- You will have invested R 290 000

- You will have R 1 756 081 today

- Your profit would be R 1 260 725,34 (tax and initial investment deducted)

Conclusion

I am fully aware that we are comparing apples and pears. With these numbers, who would not want to invest in Bitcoin? The issue here is that this data is skewed – very few people will have the knowledge or data available to invest this much money in BTC.

We all need to remember that past performance can never indicate future performance, yet people ask for historical data, and so the financial fundis give the people what they ask for.

Be careful what you invest in.

Don’t just gamble with your money.

In the same way, leveraging property is profitable, but there is a level of knowledge required. If you do this recklessly, you will die a slow and painful death. Read my other posts on property and emergency funds – have all of these in place in case something terrible happens!

Invest wisely and happy investing.