WARNING! This is a technical article riddled with opinions

Note that this is not light reading – I am exceptionally biased and this is my opinion. Enjoy the ride!

So you own the ultimate diversified ETF

What’s an ETF?

If you don’t have a clue what an ETF is, why not check my article here?

In the personal finance community, you will often find enthusiasts lamenting ETFs. The claims include quotes like “ETFs are the ultimate form of a diversified portfolio”

If you read their blog scriptures, you will find texts like:

No stock or bond shall prosper against my ETF

or:

But I tell thee: though you walk through the valley of the uninformed, thy MSCI World and thy S&P 500 shall be thy rod and thy staff

All jokes aside, I want to discuss the following in this article:

- If ETFs are seen as a well-diversified portfolio, what if history did repeat itself (crashes or an Act of God)?

- How sure are you that your ETF is diversified?

The stock market is not a diversified investment

As any reader will know, I am exceptionally biased towards investment property, and this post is no exception. I want to make it clear that I don’t believe that people should invest their life savings in one single asset class.

Imagine now if you invested your life savings in 5-10 stocks.

Now, imagine if you invested your life savings in 5-10 ETFs or funds.

And then the stock market crashed.

For me, this indicates that the stock market is a single asset class.

History repeats itself

The solar storm of 1859

As a quick lesson in history, let’s travel back in time to 1859. The sun decided to have a massive explosion (a solar storm). Even though the flares missed the earth by 9 days, the effect was quite devastating. This included telegraph systems going down – some even getting an electric shock.

Studies have shown that if this would happen today, the damage would be between $0.6–2.6 trillion in the US alone. With a total GDP of less than $ 20 trillion, this would be devastating.

Note that the only proof about who owns what is found in our computer systems. What would happen if these fries were like McDonald’s chips?

Though many might say that this as an ‘act of God’ has such a small chance of happening, we can all be reminded of the ‘Black Swan’ events. No one thought that Bernie Madoff could pull off the biggest Ponzi scheme in history – a full $65 billion.

We need to realise that we live in an era where the impossible happens.

It always seems impossible until it’s done.

-Nelson Mandela

The crash of Wall Street – 1929

Though we cannot go into details of why the market crashed, it would be beneficial to see the effect that it had on the indexes of the day.

Looking at the charts graciously stolen from here, one can see that the crisis took 25 years to reach the 400 mark again. It’s important to note that the Dow Jones Industrial Average is one of the most well-known indexes and is also seen as a barometer of international sentiment and confidence.

In hindsight, we can conclude that anyone who had their savings in most of the top stocks in the US for that time, would’ve had very little capital growth.

One can merely imagine how many people lost their life savings in actively managed funds and ETFs tracking top companies on the stock market.

It is important to consider that this is an oversimplification of a very complex set of data, including a world war, plagues and death, a bank pandemic and so forth. It does make for great scepticism relating to people telling you “what goes down must come up”.

We know that 1929 created many many millionaires in the US with the crash – yet most passive investors were not so lucky!

But I love ETFs…?

Frugal’s opinion:

I am a big fan of ETFs as a form of diversification.

I invest quite a bit of money in ETFs.

My concern I am raising here is that people swear by ETFs and the stock market. This seems to be similar behaviour that was seen just before an economic bubble (Check out Irrational Exhuberence for more info on this).

My message from this is strong: make sure you have other investments outside of the stock market. Though one can say historically the stock market has outperformed all other asset classes, I want to make sure the following is understood:

- The stock market is paper assets, which does not mean diversification

- If one would ask a person in 1955 if the stock market outperformed all other asset classes, it would’ve been a resounding no.

The S&P 500

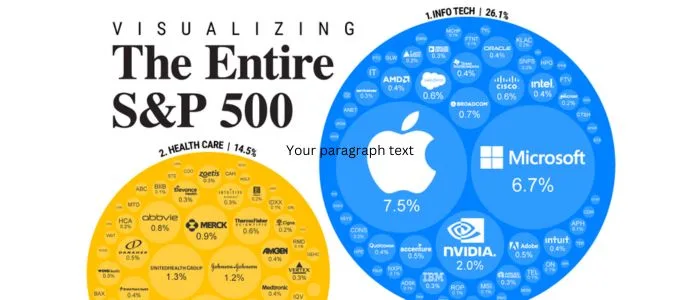

Let’s take a quick look at the S&P 500 – one of my favourite indexes.

On the pie chart one can see that the S&P 500 is overexposed to the US market.

On first glance, we can see that the S&P 500 contains many different stocks (check the Wikipedia link here). What an awesome diversification of your money! From my calculations, about 17% of the index is directly exposed to tech giants. Digging a bit deeper, one can see that many of these companies actually are indirectly exposed (e.g. financial and services and even health care to a big extent ) to the tech sphere.

It’s exceptionally important to make sure that your whole net worth is not tracking only one index or multiple indexes with similar exposure!

Diversification factors to consider

So, we’ve looked at the S&P 500.

We have also looked at how things can go awry – though we would think it never possible!

Let’s focus next on what true diversification looks like.

Diversification within your ETFs

An ETF normally tracks an index. This is helpful in so many ways, which include lowering costs of active trading, stability and unemotional decision making and easy selection of one fund into many different stocks.

Though it does count as diversification to invest in different types of stocks, no one can deny a trend where certain types of companies rise to power at a certain time. It’s also noteworthy that certain indexes are by design overexposed to certain countries or industries – or businesses of a certain size.

Investing in large corporates that you trust

One could easily claim that large indexes such as the S&P 500, MSCI World and JSE Top 40 invest in companies that often find themselves facing the innovator’s dilemma. This refers to a choice that they have to make: investing in something that will make them money now, or in something that will only bring forth fruit in the next 10-20 years.

Middle management is trained to choose money now at the cost of money later.

In this scenario, you would be missing the true growth found in disruptive innovation. On the contrary, you will be getting the bits of sustaining innovation and eventually only get the benefit once the disruptive company is not that profitable anymore.

What does true diversification look like?

Though you might think “how is this humanly possible to be diversified?!”, yeah, it’s impossible.

In my opinion one should aim for diversification in considering the following factors:

- Diversify in all asset classes, not just the stock market

- Online and offline – buy cold hard assets and paper assets

- On the stock market and off the stock market

- Invest in South Africa and other countries abroad (not just the US)

- Invest in different industries that are not related – e.g. don’t buy technology and financial stocks that could be interdependent

- Don’t buy single stocks or only one property with your entire life savings

- Consider 1-3 % of your portfolio for speculative assets

Conclusion

Though this article might sound like I am criticising the personal finance community, this is not the end goal.

I tried to highlight the absurdity in the advice that you need to push every last cent you own into ETFs stock market.

I love how people claim it’s proven that stocks have historically outperformed every single asset class, yet add with a caution ‘past performance does not indicate future performance.

Please don’t be stupid.

Invest in a real diversified portfolio.

Happy investing!